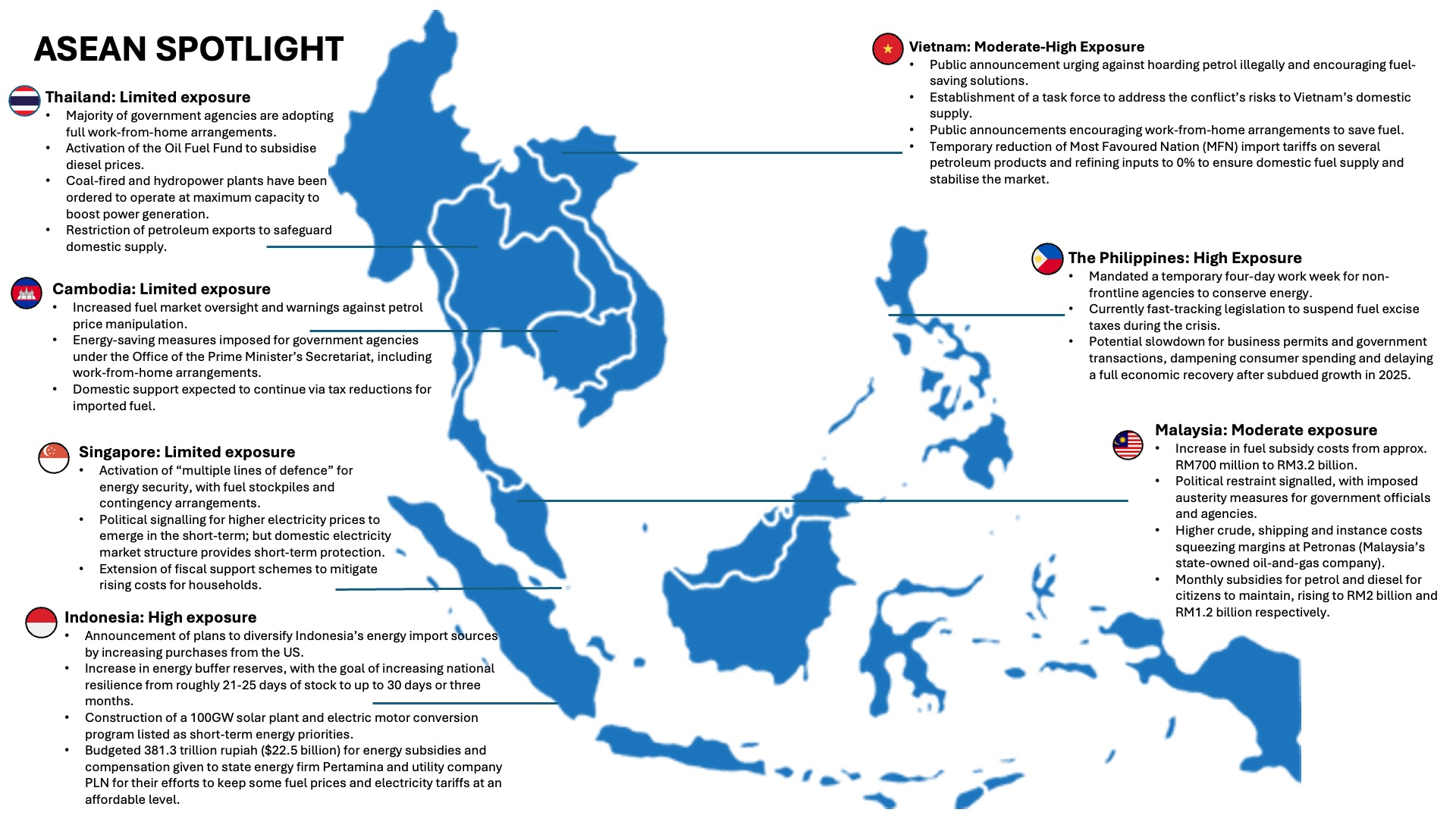

As the conflict between United States, Israel and Iran disrupts roughly 20% of global oil flows (notably through the Strait of Hormuz), the immediate shocks (i.e. price spikes, rationing and emergency releases by the International Energy Agency) are obvious.

Energy security as national security

For ASEAN, however, the crisis does more than raise costs: it reframes the region’s energy transition as a security and resilience imperative. Many ASEAN economies remain exposed to imported fossil fuels and fragmented grids, so renewables and smarter regional planning are now as much about reducing import risk as cutting emissions. ASEAN’s Economic Ministers have since affirmed their commitment to keeping markets open and strengthening energy security, emphasising the need to manage consumption, diversify energy sources and supply routes, and enhance regional cooperation on energy preparedness and cooperation on reserves. Specifically, the regional bloc called for continued collaboration on ASEAN’s already-established energy cooperation frameworks (i.e. the ASEAN Framework Agreement on Petroleum Security (APSA), the ASEAN Power Grid (APG) Enhanced Memorandum of Understanding, and the Trans-ASEAN Gas Pipeline (TAGP)).

ASEAN Power Grid: Partial or Catch-All Solution?

Since 2007, the ASEAN Power Grid (APG) has transformed from an abstract regional ambition to a financing and operational priority that can reshape energy costs, supply security and investment flows across the bloc. While it’s been designed to connect national electricity systems, the APG is also expected to buffer against global energy disruptions, where reliance now lies on shared borders, regional infrastructure, and diversification towards renewable sources instead of traditional energy sources. In practice, what this could look like include leveraging hydropower from Laos, solar energy from Thailand/Vietnam, offshore wind potential from Vietnam, and cross-border electricity imports into Singapore.

Three key dynamics surrounding the APG are quickly emerging:

- Energy security framing, where the rationale for energy transitions is accelerated not only by climate goals, but by the security of supply. In this respect, the APG satisfies the region’s internal moves towards local and regional energy source supply.

- Diversifying power supplies. Considering the volatility of today’s geopolitical climate, Southeast Asia is increasingly aware of its vulnerabilities to external shocks, especially for energy that is necessitated to power daily life. Regional electricity trade via the APG is one solution to this challenge and has proved attractive to ASEAN governments despite sovereignty questions.

- Infrastructural urgency persists. The APG as a regional project, potentially provides a greater catalyst for governments to upgrade and invest in their local electricity infrastructure, reinforcing a rethink towards renewable energy sources and strategic thinking around their energy security approach.

The Energy Transition “Trilemma”

By definition, the energy transition trilemma refers to the challenge of balancing three conflicting goals: energy security, energy equity (i.e. affordability and accessibility) and environmental sustainability. In Southeast Asia, the case could be made for energy security as the primary focus, but it leaves the latter two in ambiguity for the future. Already, the trade-offs are emerging:

- High financial and technical hurdles remain, with an estimated $764 billion in power generation and transmission investment needed, including $100 billion for cross-border transmission lines alone).

- Regulatory harmonisation is moving slowly, and risks being a key impediment for integration, especially in cross-border power purchase agreements.

- While regional consensus may be positive, domestic stability is the key variable ensuring long-term success. With domestic political instability still happening occasionally in Southeast Asian countries, there is no guarantee whether the next government-of-the day will acquiesce to the vision behind the APG.

- Furthermore, the "ASEAN Way" of consensus-based decision-making hinders the development of binding, formal dispute resolution mechanisms necessary for long-term, large-scale infrastructure projects.

Cybersecurity in the APG: An underappreciated risk

With today’s advancements, cyber-attacks in regional power grids are transitioning from a peripheral IT concern to an inevitable reality that all governments are proactive on. According to the World Bank, roughly one-third of cyberattacks were concentrated on industrial control systems, with hackers often tied to nation-states and organized crime. When it comes to information security in the energy sector, the triad of confidentiality, integrity and availability remains paramount. However, unlike other sectors, availability is the most critical for power grids, as the consequences of downtime are severe (i.e. the longer the downtime, the harder it is to rebuild the grid). For a region aiming to interconnect its national electricity grids, cyberattacks could result in a negative domino effect.

While safeguards have been set in motion in some countries, how precautions shape up for the APG remains concentrated at the high level, via the ASEAN Regional CERT (Computer Emergency Response Team). Additionally, while some ASEAN countries have made strides in developing cybersecurity frameworks for critical infrastructure, others are still in the early stages of understanding and addressing the cyber risks associated with distributed energy systems (DES) which is the main technology supporting national grids. There is also a significant gap in regional cooperation and policy harmonisation on cybersecurity for DES.

Practical Pathways Ahead

In short, the pathway to a functioning ASEAN Power Grid is unlikely to be a single region-wide buildout completed all at once. It will instead depend on a series of targeted corridors that unlock the largest and most cost-competitive renewable resources in the region. Prioritising a few high-impact interconnections can help reduce political and technical complexity while creating clearer demand signals for investors and developers. Early multilateral experiments such as the Lao–Thailand–Malaysia–Singapore Power Integration Project demonstrated the potential of cross-border power trade, but also revealed how transmission constraints, cost-sharing questions and shifting political priorities can stall momentum. Moving forward, stronger frameworks for cross-border power purchase agreements and risk-sharing will be critical. Financing also remains a quiet but decisive bottleneck. Transmission infrastructure requires long investment horizons and stable policy signals, which means governments, development banks and private investors will need to work together to crowd in capital rather than rely on public funding alone.

Concurrently, energy security and domestic political considerations will continue to shape how quickly ASEAN countries embrace deeper electricity trade. ASEAN’s consensus-based approach to decision-making can slow negotiations when national priorities diverge, particularly in an era of rising economic nationalism and protectionist instincts around critical resources. While cross-border power trade can reduce wholesale electricity costs over time, those savings do not automatically translate into lower consumer bills. Tariff structures, subsidies and existing domestic generation contracts determine whether households benefit from the APG. Maintaining public support therefore requires transparent market design and a broader narrative that connects interconnection projects to economic development, resilience and regional cooperation. Lessons from other large energy infrastructure initiatives suggest that success often comes from designing projects to be modular and scalable so that individual corridors can operate independently while gradually expanding. Embedding the ASEAN Power Grid within a wider vision of regional economic integration may ultimately prove just as important as the technical connections themselves.

Conclusion

FAQ: ASEAN's Energy Transition Realities & The APG

Q: Why is the ASEAN Power Grid (APG) critical for regional energy resilience?

A: The APG transforms regional energy strategy from an abstract ambition into an operational necessity. By connecting national systems, it buffers against external supply shocks, diversifies power sources (e.g., leveraging hydropower from Laos and offshore wind from Vietnam), and reduces the bloc's over-reliance on traditional imported fossil fuels.

Q: What is the energy transition "trilemma" facing Southeast Asia?

A: The trilemma involves the complex challenge of balancing energy security, energy equity (affordability and accessibility), and environmental sustainability. Currently, ASEAN prioritizes energy security, which creates significant financial and regulatory trade-offs, including an estimated $764 billion needed for power generation and transmission investments.

Q: How are cyber threats impacting ASEAN’s energy infrastructure?

A: Cyberattacks on industrial control systems are shifting from peripheral IT concerns to severe threats capable of causing negative domino effects across interconnected grids.

- There is currently a significant gap in regional policy harmonization regarding cybersecurity for distributed energy systems (DES), making grid availability highly vulnerable.

Q: What are the primary bottlenecks preventing rapid APG integration?

A: The primary bottlenecks include a massive financing gap, slow regulatory harmonization for cross-border power purchase agreements, and domestic political instability.

- Additionally, ASEAN’s consensus-based decision-making approach complicates the creation of formal dispute resolution mechanisms required for long-term, large-scale infrastructure projects.

Q: How can Speyside help your company navigate ASEAN's energy transition realities?

A: Speyside assists companies by navigating the complex regulatory harmonization and political hurdles inherent in ASEAN's diverse markets. We provide critical intelligence on targeted energy corridors, support the structuring of cross-border power purchase agreements, and ensure your market entry strategies align with both national energy security priorities and broader regional economic integration efforts.

For more information please contact:

Matthew Lloyd

Regional Director Europe, Middle East & Affrica

Matthew.lloyd@speyside-group.com